Understanding the Borrowing Process: Exploring the Steps to Acquiring Funds

One of the most important aspects of financial planning is understanding the borrowing process and the steps involved in acquiring funds. Whether you are looking to finance a major purchase, start a business, or deal with unexpected expenses, knowing how to borrow money effectively can make a significant difference in achieving your financial goals.

The first step in the borrowing process is to determine your funding needs. This involves evaluating the specific purpose for which you require funds and estimating the amount of money you will need. Whether it’s for buying a house, paying for education, or consolidating debts, having a clear understanding of your financial goals will help you determine the amount you need to borrow and make informed decisions when selecting the most suitable borrowing option. Additionally, it is essential to conduct thorough research to compare various lenders, their interest rates, and loan terms to identify the best deal that aligns with your financial situation and objectives. The borrowing process can be complex, but by following these steps, you can navigate it effectively and make informed decisions to access the funds you need.

Factors to Consider Before Applying for a Loan: Assessing Your Financial Situation

Before applying for a loan, it is crucial to assess your financial situation to determine if you are in the right position to take on additional debt. First and foremost, take a close look at your income and expenses. Calculate your monthly income and subtract all your necessary expenses such as rent or mortgage payments, utility bills, and groceries. This will give you a clear picture of how much disposable income you have each month and if you can afford to make loan repayments without sacrificing your essential needs.

In addition to your income and expenses, it is important to evaluate your credit history. Lenders consider your credit score when determining your eligibility for a loan. Therefore, obtain a copy of your credit report and review it for any errors or discrepancies. Pay close attention to your payment history, debt utilization, and the length of your credit history. If you have a low credit score, you may need to work on improving it before applying for a loan or consider alternative options such as a secured loan. Taking the time to assess your financial situation thoroughly will help you make an informed decision and ensure that you are financially prepared to take on a loan.

Different Types of : Exploring the Options Available to You

When it comes to personal loans, it’s essential to understand that there are various options available to suit your specific needs. Each type of personal loan comes with its own set of features, requirements, and repayment terms. One common type is an installment loan. With this type of loan, you borrow a fixed amount of money upfront and repay it in equal monthly installments over a set period. Installment loans are popular for larger purchases such as buying a car or financing home improvements. Another option is a revolving line of credit. This type of loan allows you to borrow funds up to a predetermined limit whenever you need them. As you repay the borrowed amount, the available credit replenishes, providing you with flexibility for ongoing expenses or emergencies.

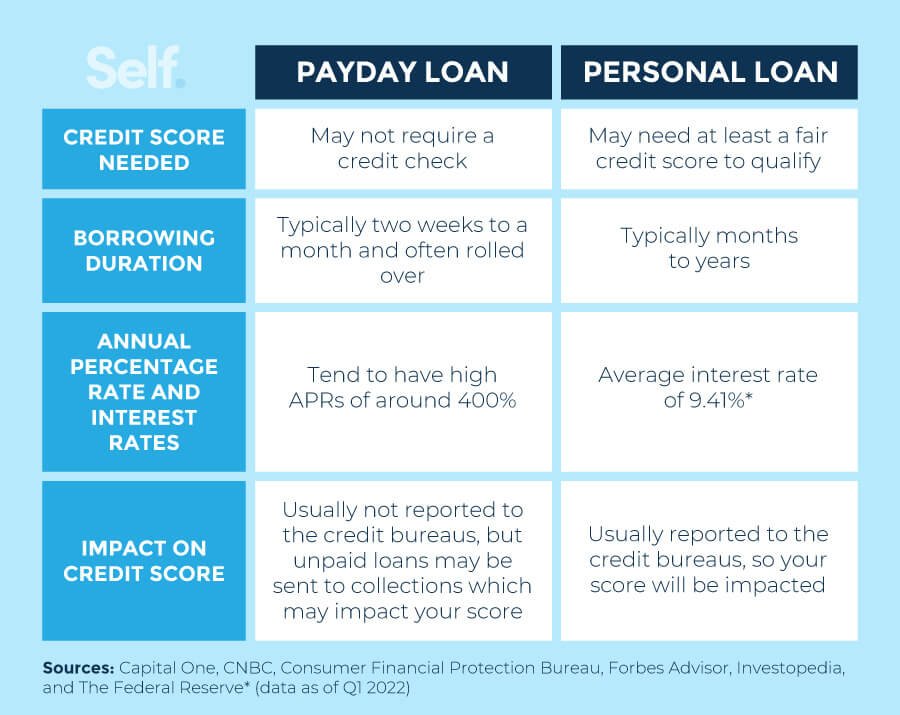

Another type of personal loan is a payday loan. Payday loans are typically small, short-term loans designed to cover unexpected expenses until your next paycheck. These loans often come with high interest rates and fees, so it’s important to carefully consider your ability to repay them before borrowing. Additionally, if you’re a homeowner, you may have the option to consider a home equity loan or a home equity line of credit. These loans use the equity you have built in your home as collateral and can be used for a variety of purposes, such as debt consolidation or major expenses. It’s important to note that failure to repay a home equity loan may result in the loss of your home. As you explore the different types of personal loans available, carefully consider your financial situation and borrowing needs to make an informed decision that suits your goals and ensures responsible financial management.

The Importance of Credit Scores: How Your Credit History Affects Loan Eligibility

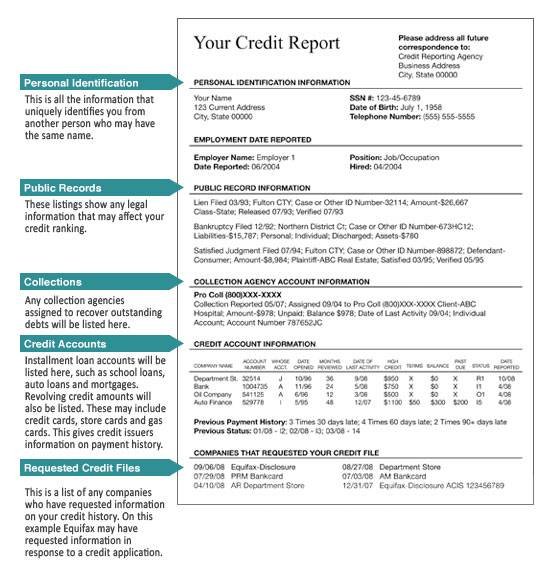

Having a good credit score is crucial when it comes to loan eligibility. Lenders rely heavily on credit scores to determine the risk associated with lending money to individuals. A credit score, typically ranging from 300 to 850, is a numerical representation of an individual’s creditworthiness. It takes into account factors such as payment history, outstanding debts, length of credit history, and types of credit used. A higher credit score indicates a lower risk borrower, making it easier to qualify for loans and secure better interest rates.

Your credit history is a detailed record of your borrowing and payment behavior. It includes information about all credit accounts you have open or have had in the past, including credit cards, mortgages, auto loans, and personal loans. Lenders use this information to evaluate your creditworthiness and determine how likely you are to repay your debts on time. A positive credit history, with a track record of making payments on time and keeping debt levels low, can significantly improve your chances of loan approval. Conversely, a negative credit history, with late payments, defaults, or high amounts of debt, can make lenders hesitant to offer you a loan or may result in higher interest rates and stricter terms.

Comparing Interest Rates and Loan Terms: Finding the Best Deal for Your Needs

When comparing interest rates and loan terms, it is crucial to carefully evaluate all available options in order to find the best deal for your needs. Interest rates represent the cost of borrowing money and can significantly impact the total amount you repay over time. Therefore, it is wise to compare and consider different interest rates offered by various lenders. By doing so, you can identify the most competitive rates that align with your financial situation and repayment capabilities.

In addition to interest rates, loan terms should also be taken into account when comparing different borrowing options. Loan terms refer to the length of time you have to repay the loan. It is important to choose a term that suits your financial goals and ensures a manageable repayment schedule. Shorter loan terms often come with higher monthly payments but can save you money in the long run by reducing the overall interest paid. On the other hand, longer loan terms may result in lower monthly payments but could also mean paying more in interest over the life of the loan. Taking the time to evaluate both interest rates and loan terms will help you find the best deal that meets your financial needs and objectives.

Secured vs Unsecured Loans: Understanding the Difference and Implications

Secured loans and unsecured loans are two common types of borrowing options available to individuals. The main difference between the two lies in the collateral requirement. Secured loans are backed by collateral, which can be an asset such as a car, house, or savings account. This collateral serves as a guarantee for the lender that they will be able to recover their money if the borrower fails to repay the loan. Consequently, secured loans generally have lower interest rates compared to unsecured loans.

On the other hand, unsecured loans do not require collateral. Instead, lenders rely solely on the borrower’s creditworthiness to determine their eligibility for the loan. These loans are typically offered based on the borrower’s income, credit history, and employment status. Since there is no collateral involved, unsecured loans pose a higher risk for lenders, resulting in higher interest rates than secured loans. It is important for borrowers to carefully consider their financial situation and ability to repay before deciding between the two types of loans.