Understanding Payday Loans: Exploring the Basics

Payday loans have gained significant attention in recent years, sparking debate and controversy. These short-term loans are often marketed as a quick and convenient solution for individuals facing unexpected financial emergencies. However, it is crucial to understand the basics of payday loans before considering them as an option.

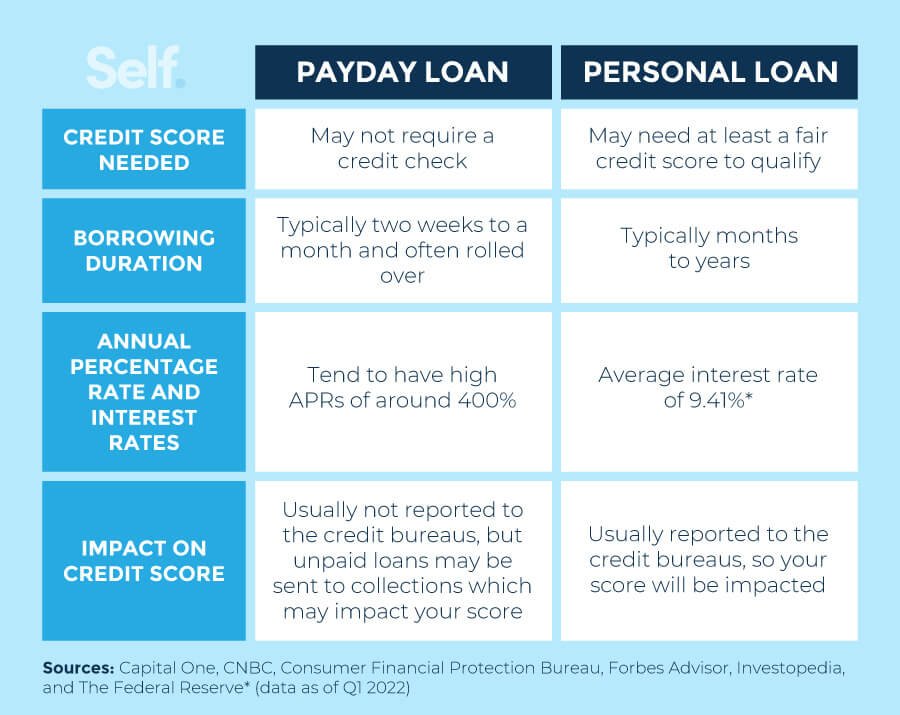

Unlike traditional bank loans, payday loans are typically smaller in amount and have a shorter repayment period, usually due on the borrower’s next payday. They are designed to provide quick access to cash, with minimal requirements and a simple application process. Borrowers are often required to provide proof of income, a valid ID, and a post-dated check or pre-authorization for electronic repayment. Interest rates for payday loans are considerably higher than those of traditional loans, often reaching triple-digit Annual Percentage Rates (APRs). It is essential to carefully evaluate the terms, fees, and potential risks associated with payday loans before making a decision.

Understanding the basics of payday loans is an essential step in making informed financial decisions. While they may seem like a convenient option, it is crucial to consider the potential impact on your overall financial health. In the following sections, we will explore the key features and terms of payday loans, evaluate their pros and cons, and compare them with traditional bank loans. By examining the alternatives available for short-term cash needs, you will be better equipped to make a wise and well-informed choice that aligns with your financial goals and circumstances.

Key Features and Terms of Payday Loans

When considering payday loans, it is essential to understand their key features and terms. These loans are typically short-term, small-dollar loans that are meant to be repaid in full on the borrower’s next payday. They are often sought by individuals who are facing unexpected financial emergencies or who may not have access to traditional forms of credit. One of the main features of payday loans is their accessibility, as they are relatively easy to obtain with minimal requirements. However, this accessibility comes at a cost, as payday loans often carry high-interest rates and fees, resulting in a higher overall cost for borrowers.

In terms of repayment, payday loans usually require the borrower to provide a post-dated check or authorization for electronic withdrawal, ensuring that the lender receives payment on the agreed-upon date. If the borrower is unable to repay the loan in full on the due date, additional fees or interest may be incurred, leading to a cycle of debt for some individuals. Additionally, payday loans may have terms and conditions that differ from traditional bank loans, including shorter repayment periods and stricter eligibility criteria. Understanding these key features and terms is crucial when considering whether a payday loan is the most suitable option for one’s financial needs.

Evaluating the Pros and Cons of Payday Loans

Payday loans have become a popular option for individuals who find themselves facing unexpected financial emergencies. These short-term loans are designed to provide borrowers with instant cash to cover immediate expenses until their next paycheck. Despite their convenience, payday loans come with a set of pros and cons that need careful consideration.

One of the advantages of payday loans is their accessibility. Traditional bank loans often require extensive paperwork and a lengthy approval process, making them unsuitable for urgent financial needs. Payday loans, on the other hand, have minimal eligibility requirements and can be obtained quickly and easily. Additionally, payday loans do not typically require a credit check, making them available to individuals with poor or no credit history. This can be a significant benefit for those who have been turned away by traditional lenders.

The Impact of Payday Loans on Borrowers’ Financial Health

Payday loans can have a significant impact on the financial health of borrowers. These short-term loans, also known as cash advances or paycheck advances, are designed to provide quick access to funds for individuals facing unexpected expenses or cash flow problems. While they may seem like a convenient solution at first, payday loans often come with high interest rates and fees that can trap borrowers in a cycle of debt.

One of the main reasons why payday loans can negatively affect borrowers’ financial health is the high cost associated with these loans. Lenders typically charge exorbitant interest rates, sometimes reaching triple digits on an annual percentage rate (APR) basis. Additionally, borrowers are often required to repay the loan in a single lump sum, usually within a few weeks. This can create a significant burden, especially for those who are already struggling to make ends meet. As a result, borrowers may find themselves unable to repay the loan on time and may be forced to roll over the loan, incurring additional fees and interest. This cycle can quickly spiral out of control, leading to a never-ending cycle of borrowing and debt.

Comparing Payday Loans with Traditional Bank Loans

Traditional bank loans and payday loans are two popular options for individuals seeking short-term financial assistance. However, these two types of loans differ significantly in their terms and conditions, eligibility criteria, and overall impact on borrowers’ financial health.

One key distinction between payday loans and traditional bank loans lies in the borrowing process. When applying for a traditional bank loan, individuals are typically required to submit extensive documentation, including proof of income, credit history, and collateral. The loan approval process can be time-consuming and involves a thorough assessment of the borrower’s financial background. On the other hand, payday loans are often characterized by a simpler application process, with minimal documentation requirements. These loans are designed to provide quick cash to borrowers with limited credit history or poor credit scores.

Exploring Alternatives to Payday Loans for Short-Term Cash Needs

When faced with an urgent need for short-term cash, many individuals turn to payday loans as a quick solution. However, it is important to explore alternative options that may offer better terms and lower interest rates. One such alternative is seeking assistance from local nonprofit organizations that provide financial assistance or emergency grants. These organizations can offer support by providing funds to cover immediate expenses or connecting individuals with resources to meet their specific needs. Additionally, exploring community-based programs or government assistance programs can provide short-term financial relief, allowing individuals to avoid the high interest rates and fees associated with payday loans.

Another alternative to consider is borrowing from friends or family members. While this may not be an option for everyone, it is worth exploring if one has a reliable support system. Borrowing from loved ones can often come with more flexible repayment terms, lower or no interest rates, and greater understanding of individual circumstances. However, it is crucial to approach these arrangements with professionalism and to ensure clear communication and mutually agreed-upon terms in order to maintain healthy relationships.