Factors Affecting Loan Risk Assessment

When it comes to loan risk assessment, there are several key factors that lenders consider in order to determine the level of risk associated with a particular borrower. One of the most important factors is the borrower’s creditworthiness, which is typically assessed by reviewing their credit history and credit score. Lenders use this information to gauge the borrower’s ability and likelihood to repay the loan based on their past financial behavior. A borrower with a low credit score or a history of missed payments may be viewed as a higher risk, while a borrower with a high credit score and a strong repayment history may be seen as a lower risk. Additionally, lenders also take into account the borrower’s income, employment stability, and debt-to-income ratio, as these factors provide further insight into the borrower’s financial capacity to repay the loan. By carefully evaluating these factors, lenders can make more informed decisions about loan risk and potential default.

Another crucial factor in loan risk assessment is the analysis of interest rates and loan terms. Lenders carefully consider the interest rate associated with the loan, as a higher rate increases the risk of default. Additionally, the length of the loan term can also impact risk assessment. Longer loan terms may increase the likelihood of default, as the borrower is exposed to a greater number of potential risks over an extended period of time. On the other hand, shorter loan terms may decrease the risk of default, as the borrower has a smaller window of opportunity to encounter financial difficulties. By evaluating the interest rates and loan terms, lenders can assess the level of risk associated with a loan and make adjustments accordingly.

Evaluating Borrower’s Creditworthiness

Lenders face a critical challenge when assessing the creditworthiness of borrowers. This process involves examining various factors that indicate the borrower’s ability and willingness to repay their loan obligations in a timely manner. One of the primary factors taken into consideration is the borrower’s credit score. A credit score is a numerical representation of an individual’s creditworthiness, reflecting their credit history, payment behavior, and levels of debt. Lenders typically rely on credit reports from credit bureaus to obtain the borrower’s credit score and assess their creditworthiness. A higher credit score indicates a lower risk of default, while a lower score may raise concerns about the borrower’s ability to fulfill their financial obligations. Furthermore, lenders may also consider the borrower’s credit utilization ratio, which measures the extent to which they are using available credit. High credit utilization can be an indicator of potential financial strain and may impact the borrower’s creditworthiness. Ultimately, evaluating a borrower’s creditworthiness is a crucial step in mitigating lending risks and ensuring the overall stability of the lending institution.

In addition to credit scores and credit utilization, lenders also analyze the borrower’s credit history. This involves reviewing the borrower’s past payment patterns and any derogatory marks, such as late payments, foreclosures, or bankruptcies. A clean credit history with consistent on-time payments boosts the borrower’s creditworthiness, signaling their reliability in meeting financial obligations. However, a tarnished credit history can raise concerns for lenders, as it suggests a higher probability of default. To further assess creditworthiness, lenders may also consider the borrower’s debt-to-income ratio. This ratio compares the borrower’s monthly debt obligations to their monthly income, providing an indication of their ability to take on additional debt. A lower debt-to-income ratio implies a greater capacity to repay new loans, while a higher ratio may signify financial strain and increased risk for lenders. By evaluating these various aspects of the borrower’s creditworthiness, lenders can make informed decisions and determine suitable terms for loans, ensuring a balanced and responsible lending approach.

Exploring Different Types of Loans

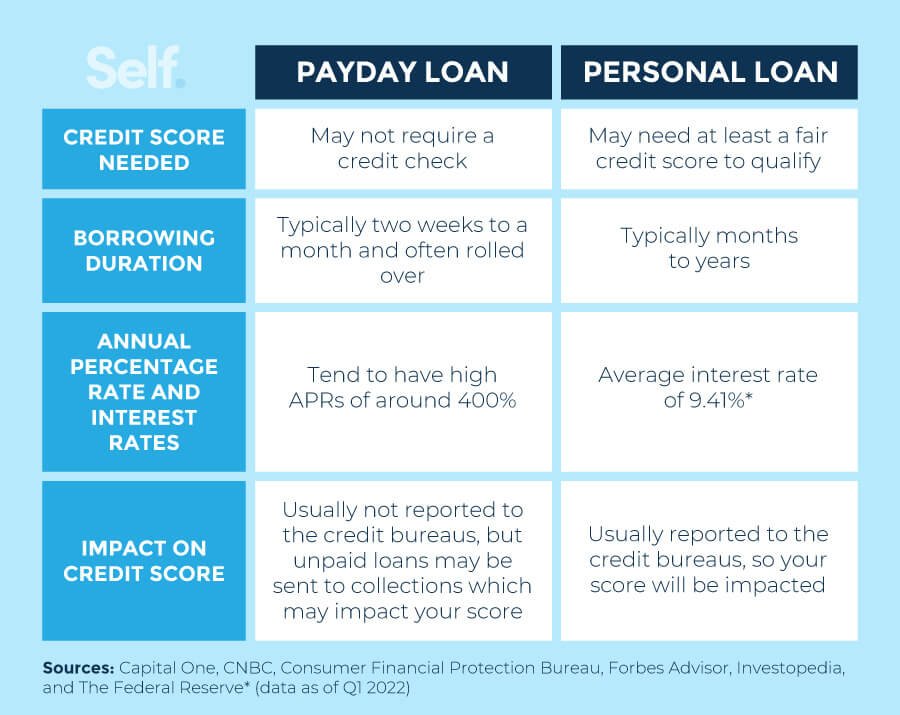

There are numerous types of loans available in the financial market, each designed to cater to different needs and circumstances. One commonly known type is a personal loan, which can be used for various purposes such as consolidating debt, financing a vacation, or covering unexpected expenses. Personal loans typically have a fixed interest rate and repayment period, making them a popular choice for those seeking flexibility and convenience.

Another type of loan is a mortgage loan, which is specifically designed for purchasing or refinancing a home. Mortgage loans often come with different interest rate options, such as fixed or adjustable rates, and may require a down payment or collateral like the property itself. Due to the long repayment term and significant loan amount involved, careful consideration and financial planning are essential when exploring mortgage loan options. Understanding these various loan types and their particular features can help borrowers make informed decisions based on their specific financial goals and circumstances.

Analyzing Interest Rates and Loan Terms

When evaluating loan options, it is crucial to carefully analyze the interest rates and loan terms offered by different lending institutions. The interest rate is the cost of borrowing money and can vary significantly from one lender to another. It is essential to compare interest rates to ensure that the borrower is obtaining the most favorable terms available. Additionally, the loan terms, such as the duration of the loan and any associated fees, play a crucial role in determining the overall cost of the loan. Borrowers should review these terms meticulously and consider their ability to meet the payment obligations before committing to any loan agreement.

Interest rates can have a substantial impact on the overall cost of a loan. A higher interest rate means that the borrower will be paying more in interest over the loan’s term, resulting in higher monthly payments. Conversely, a lower interest rate can significantly reduce the cost of borrowing and provide lower monthly payments. It is important to note that interest rates can be influenced by various factors, including the borrower’s creditworthiness, the loan type, and prevailing market conditions. By analyzing interest rates and loan terms thoroughly, borrowers can make informed decisions, minimize costs, and choose the loan that best aligns with their financial goals.

Assessing Collateral and Loan-to-Value Ratios

One crucial aspect of assessing loan risk is evaluating the collateral that borrowers are offering to secure the loan. Collateral refers to an asset or property that the borrower pledges to the lender as a form of security. In the event that the borrower fails to repay the loan, the lender can seize the collateral to recover their losses. When assessing collateral, lenders consider factors such as the type and value of the asset, its market liquidity, and its susceptibility to depreciation. By thoroughly evaluating the collateral, lenders can determine its adequacy in covering the loan amount and mitigating potential risks.

Understanding the Impact of Economic Conditions on Loan Risks

In the world of lending and borrowing, economic conditions act as a powerful force that can significantly impact the level of risk associated with loans. The state of the economy, including factors such as inflation rates, interest rates, and overall market stability, can greatly influence the ability of borrowers to repay their loans. Moreover, economic conditions can also affect the value of collateral and the loan-to-value ratios, further impacting the risk assessment process.

During times of economic prosperity and stability, borrowers generally have a higher likelihood of repaying their loans on time. This is because job security tends to be higher, incomes are stable, and overall consumer confidence is strong. On the other hand, during economic downturns or recessions, borrowers may face financial challenges such as job loss, reduced income, or increased cost of living. These factors can lead to a higher likelihood of default and, consequently, increase the risk associated with lending.