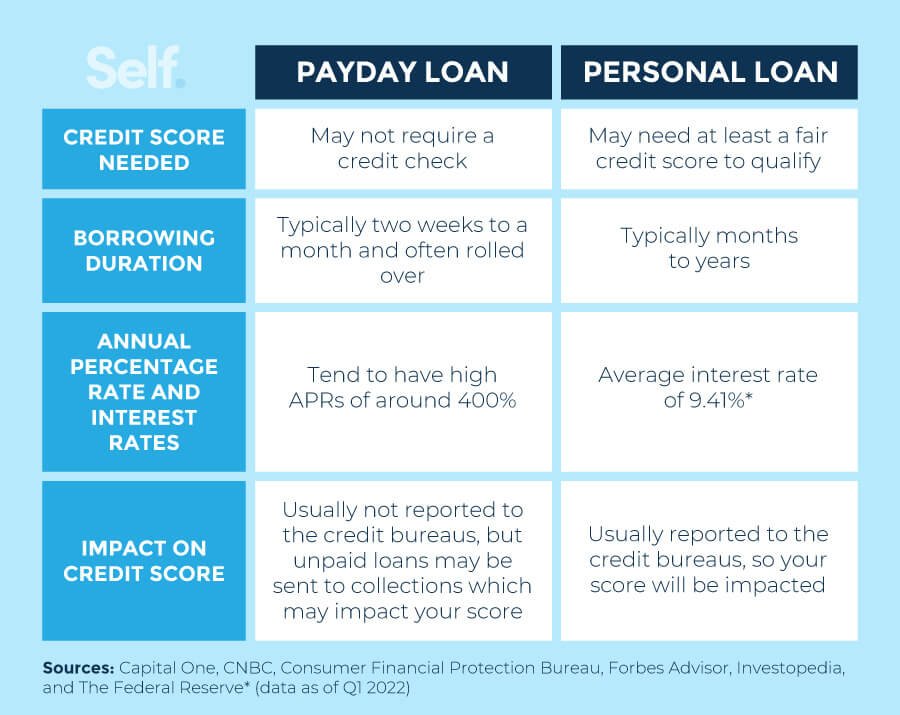

The Pitfalls of Payday Loans

Payday loans can be enticing for those in need of quick cash, but they can also be a dangerous trap. One of the main pitfalls of payday loans is the exorbitant interest rates they often carry. With annual percentage rates (APRs) that can reach up to 400% or higher, borrowers can find themselves in a cycle of debt that is difficult to escape. These loans are typically repaid within a few weeks, leading many borrowers to take out new loans to cover the old ones, creating a cycle of dependency.

Another pitfall of payday loans is the lack of regulation and transparency in the industry. Many payday lenders prey on vulnerable individuals with limited financial literacy, often glossing over the terms and conditions of the loan. This can result in borrowers unknowingly signing up for loans with hidden fees and penalties, making it even more challenging to break free from the debt cycle. Additionally, these lenders often do not perform thorough credit checks, which can lead to borrowers taking on loans that they cannot afford to repay.

Building a Strong Financial Foundation: Budgeting and Saving Tips

Building a strong financial foundation is essential for long-term financial stability and success. One of the most effective ways to achieve this is through budgeting and saving. By creating a budget, individuals can track their income and expenses, ensuring that they are living within their means and saving for future goals. This includes setting aside a portion of income for necessities, such as housing and groceries, as well as for discretionary spending and saving.

In addition to budgeting, saving is a crucial component of building a strong financial foundation. By regularly setting aside money in a savings account, individuals can create an emergency fund to cover unexpected expenses, such as medical bills or car repairs. Saving also allows for the pursuit of long-term financial goals, such as buying a home or funding retirement. By prioritizing budgeting and saving, individuals can lay the groundwork for a solid financial future and achieve greater financial security.

Exploring Credit Union Options for Short-Term Loans

Credit unions are often overlooked when it comes to short-term loans, but they can be a valuable resource for individuals in need of quick cash. Unlike traditional banks, credit unions are member-owned and operated, which means they are often more flexible and willing to work with their members to find the best loan options. Many credit unions offer short-term loans with lower interest rates and more favorable terms than payday lenders. Additionally, credit unions prioritize financial education and support, providing resources and guidance to help their members improve their financial well-being.

When exploring credit union options for short-term loans, it’s important to consider the eligibility criteria and requirements. While credit unions are typically more lenient than traditional banks, they still have certain guidelines in place. Generally, individuals need to become members of the credit union to access their loan products. This may involve meeting certain residency or employment criteria, as well as opening a savings account. By becoming a member of a credit union, individuals not only gain access to short-term loan options but also a wide range of other financial services, such as low-interest credit cards, savings accounts, and financial planning assistance.

In conclusion, credit unions are a viable alternative to traditional banks and payday lenders when it comes to short-term loans. With their member-focused approach, credit unions provide more flexible options and better terms for borrowers. By exploring credit union options, individuals can not only find the financial assistance they need but also become part of a supportive community that prioritizes their financial well-being.

Tapping into Community Resources: Nonprofit Organizations that Offer Financial Assistance

Nonprofit organizations play a vital role in providing financial assistance to individuals and families in need. These community resources are dedicated to supporting those facing economic hardships by offering various forms of aid. From emergency funds to utility bill assistance, these organizations aim to alleviate financial burdens and provide relief to those struggling to make ends meet.

One of the major benefits of tapping into nonprofit organizations for financial assistance is the wide range of services they offer. These organizations understand that financial difficulties can stem from various factors, such as unexpected medical expenses or job loss. As a result, they provide assistance in the form of rent and mortgage assistance, food banks, educational grants, and even counseling services to help individuals navigate through challenging financial situations. By accessing these resources, individuals and families can find the support they need to regain stability and work toward a brighter financial future.

Negotiating with Creditors: How to Consolidate and Settle Debts

When facing overwhelming debt, negotiating with creditors can be a viable option for individuals seeking to consolidate and settle their debts. Consolidation involves combining multiple debts into a single payment, often with a lower interest rate and more manageable terms. To begin the negotiation process, it is crucial to gather all relevant financial information, including outstanding balances, interest rates, and any penalties or fees. This information can help in determining the best approach to negotiating with creditors, whether it be through debt consolidation programs, debt settlement arrangements, or working directly with creditors to create a repayment plan. It is essential to approach negotiations with professionalism and a clear understanding of one’s financial situation, expressing a willingness to work towards a mutually beneficial solution. Utilizing the services of a professional debt counselor or financial advisor can provide guidance and expertise throughout the negotiation process, increasing the chances of achieving a successful outcome.

After identifying the most effective negotiation strategy, it is crucial to communicate with creditors in a clear and concise manner. When contacting creditors, maintaining a professional tone is vital, as emotions or confrontational approaches can complicate the negotiation process. Clearly state the intention to consolidate debts or settle them, providing the creditor with a proposal outlining the preferred terms of repayment. This may include requesting a reduction in interest rates, seeking a lower monthly payment, or negotiating for a lump sum settlement amount. Clearly articulating one’s financial circumstances and demonstrating a commitment to repaying the debts can help in establishing credibility and opening the door for potential negotiations. Additionally, it is essential to listen carefully to creditors’ responses and remain open to their suggestions or counteroffers. By engaging in a respectful and cooperative manner, debtors can reach mutually beneficial agreements with creditors, leading to the consolidation and settlement of their debts.

Exploring Peer-to-Peer Lending Platforms as an Alternative to Payday Loans

Peer-to-peer lending platforms have emerged as a viable alternative to traditional payday loans for those seeking financial assistance. These platforms connect borrowers directly with individual lenders, cutting out the middleman and potentially offering lower interest rates. One advantage of peer-to-peer lending is the ability to borrow larger sums of money for longer periods, allowing borrowers to cover unexpected expenses or consolidate high-interest debts.

Unlike payday loans, which often come with exorbitant interest rates and short repayment terms, peer-to-peer lending platforms offer more flexible terms and competitive rates. Borrowers can create loan listings outlining their needs and financial background, which lenders then consider before deciding whether to invest. This direct connection between borrowers and lenders provides an opportunity for individuals with less-than-perfect credit scores to secure a loan based on other factors, such as income and financial stability.

Additionally, the online nature of peer-to-peer lending means that the process is typically quick and convenient. Borrowers can apply for a loan from the comfort of their own homes, and once approved, funds can be deposited directly into their bank accounts. Furthermore, peer-to-peer lending platforms often have user-friendly interfaces and helpful customer support to guide borrowers through the loan application and repayment process.

The Benefits of Credit Card Cash Advances

Credit card cash advances can provide a convenient option for those in need of immediate funds. One of the key benefits is the quick access to cash. Unlike traditional loans, which often require lengthy approval processes, credit card cash advances allow you to withdraw money directly from your credit card. This can be particularly useful in emergency situations where time is of the essence.

Another advantage of credit card cash advances is the flexibility they offer. Once you receive the funds, you can use them for whatever you need, without any restrictions. Whether it’s covering unexpected medical expenses or addressing urgent home repairs, credit card cash advances give you the freedom to allocate the funds as you see fit. Furthermore, some credit cards even offer promotional rates for cash advances, allowing you to save on interest charges. However, it is important to remember that these rates are often temporary and usually revert to a higher APR after a certain period. Therefore, it’s crucial to carefully consider the terms and conditions before relying solely on credit card cash advances as a long-term solution.

Exploring Personal Installment Loans from Traditional Banks

Traditional banks offer personal installment loans as a viable option for individuals seeking financing for various purposes. These loans are typically structured to be repaid over a fixed period of time through regular monthly installments. One of the key advantages of personal installment loans from traditional banks is their relatively lower interest rates compared to other forms of short-term loans. This makes them an attractive option for borrowers looking for more affordable and manageable repayment terms.

In addition to the cost savings, personal installment loans from traditional banks also provide borrowers with the benefit of dealing with a well-established financial institution. This can instill a sense of trust and reliability, as these banks have a reputation for stringent lending standards and professional service. Moreover, personal installment loans from traditional banks often come with flexible loan terms and repayment plans, allowing borrowers to customize the loan to suit their specific needs and financial capabilities. This provides borrowers with a greater degree of control and ensures that the loan works in their favor rather than adding to their financial burden.

Utilizing Home Equity or Personal Assets for Emergency Funding

One option to consider when in need of emergency funding is utilizing your home equity or personal assets. If you own a home and have equity built up, you may be eligible for a home equity loan or a home equity line of credit (HELOC). These options allow you to borrow against the value of your home, using the equity as collateral.

When obtaining a home equity loan or HELOC, it’s important to keep in mind that you are putting your home at risk if you are unable to repay the loan. Additionally, there may be closing costs and fees associated with these types of loans. It is crucial to carefully evaluate your financial situation and consider the potential risks before proceeding with this option. If you don’t own a home, you may still have personal assets that could be used as collateral for a loan. This could include valuable possessions, such as jewelry, artwork, or a vehicle. Be sure to explore all possible options and compare interest rates, terms, and conditions before making a decision.

Exploring Employer-Based Loan Programs and Salary Advances

Many employers offer loan programs and salary advances as part of their benefits package. These programs can be a helpful resource for employees who find themselves in need of short-term financial assistance. By tapping into these employer-based options, individuals can access funds quickly and conveniently, without having to go through the traditional loan application process. Salary advances, in particular, allow employees to borrow against their future earnings, providing a temporary solution to their financial challenges.

One of the key advantages of exploring employer-based loan programs and salary advances is the convenience they offer. Since these options are provided by the employer, the application process is often streamlined and less time-consuming than traditional loans. Additionally, eligibility requirements may be more lenient, allowing employees with lower credit scores or limited credit history to still access the funds they need. Moreover, repayment terms are often more flexible, providing the borrower with a tailored solution that suits their financial situation. However, it is important to note that while these programs can be beneficial, they should be used responsibly and as a last resort to avoid further financial strain in the long run.