Understanding the Dangers of High-Interest Loans

High-interest loans can be incredibly risky and can easily trap borrowers in a cycle of debt. These loans typically have interest rates that are significantly higher than traditional loan options, making them appealing to those in desperate financial situations. However, while they may provide a quick solution to immediate cash needs, borrowers often find themselves struggling to keep up with the high repayments.

The dangers associated with high-interest loans are numerous. For starters, borrowers may find themselves in a never-ending cycle of borrowing and repaying. Since the interest rates are so high, borrowers may struggle to pay off the loan in full, resulting in the need to take out another loan to cover the previous one. This cycle can quickly spiral out of control, leaving borrowers drowning in debt. Additionally, the high interest rates can lead to substantial financial burden, making it difficult for borrowers to meet other essential expenses such as rent, utilities, or even groceries. As a result, individuals may find themselves in a constant state of financial stress and vulnerability.

Assessing the Impact of Payday Loans on Borrowers’ Finances

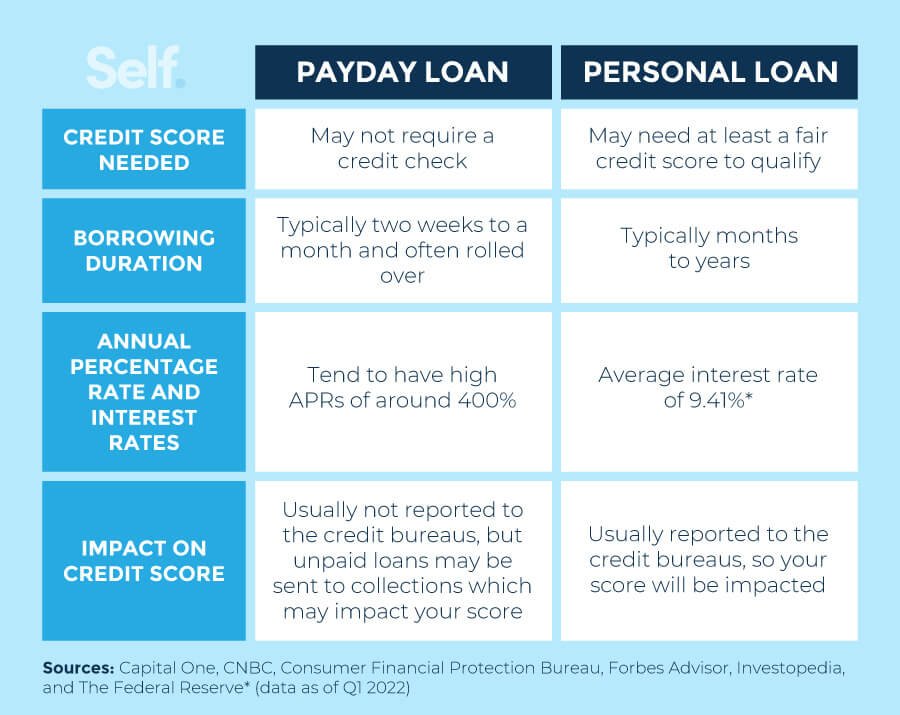

Payday loans have become a popular option for individuals in need of immediate cash, but their impact on borrowers’ finances cannot be overlooked. These loans often come with high interest rates and fees, making it difficult for borrowers to repay them in a timely manner. As a result, many borrowers find themselves trapped in a cycle of debt, borrowing more money to cover existing loans and falling deeper into financial turmoil.

The impact of payday loans on borrowers’ finances is far-reaching. Not only do borrowers face the burden of high interest rates, but they may also incur additional fees for late payments or extensions. This can have a significant impact on their overall financial situation, leading to increased levels of stress and anxiety. Furthermore, the cycle of borrowing and repaying payday loans can make it difficult for borrowers to break free from their financial struggles and stabilize their finances. Without alternative options or proper financial education, it becomes increasingly challenging for borrowers to escape this vicious cycle.

Uncovering Predatory Lending Practices in the Payday Loan Industry

The payday loan industry has long been plagued by predatory lending practices that target vulnerable borrowers. These practices take advantage of individuals who are in desperate need of short-term financial assistance, trapping them in a cycle of debt and perpetual borrowing. One of the most concerning aspects of predatory lending is the excessive interest rates charged on these loans, sometimes reaching triple digits. This exploitative tactic often leads borrowers to take out additional loans to repay their existing ones, further exacerbating their financial situation.

In addition to exorbitant interest rates, predatory lenders frequently engage in deceptive practices to entice borrowers into taking out loans they cannot afford. They will often downplay the risks associated with payday loans, emphasizing the quick and easy access to cash without adequately explaining the potential consequences. Moreover, they may employ aggressive marketing techniques, targeting individuals in financial distress and exploiting their vulnerability. These unethical practices not only deceive borrowers, but they also perpetuate a cycle of dependency on payday loans, trapping individuals in a never-ending cycle of debt.

Exploring Alternatives to Payday Loans for Financial Emergency

When faced with a financial emergency, many individuals turn to payday loans as a quick source of cash. However, these high-interest loans can often lead borrowers into a cycle of debt that is difficult to escape. It is crucial, therefore, to explore alternative options before resorting to such loans.

One alternative to payday loans is to seek help from local community organizations or charities. These organizations often provide emergency financial assistance or can connect individuals with resources in the community that can help meet their immediate needs. Additionally, many credit unions offer small-dollar loans with lower interest rates and more flexible repayment terms compared to payday lenders. By exploring these alternatives, individuals can avoid the pitfalls of high-interest loans and find more sustainable solutions for managing their financial emergencies.

Identifying Warning Signs of Debt Traps and Cycle of Borrowing

As individuals navigate their financial lives, it is crucial to be aware of the warning signs associated with debt traps and the vicious cycle of borrowing. One of the primary indications of falling into a debt trap is consistently relying on high-interest loans to cover daily expenses or meet financial emergencies. When borrowers find themselves using payday loans or other types of high-interest loans repeatedly, it is often a red flag signaling a potential debt trap.

Another warning sign to watch out for is borrowing more than what can be comfortably repaid. Taking on loans that exceed one’s ability to make regular payments can quickly lead to a cycle of borrowing, as additional loans may need to be acquired to cover existing debts. This can quickly spiral into a never-ending cycle that becomes increasingly difficult to break free from. It is important to closely monitor one’s debt-to-income ratio and ensure that loan obligations are within manageable limits to avoid being trapped in a cycle of debt.

Analyzing the Role of Government Regulations in Protecting Consumers

Government regulations play a crucial role in ensuring the protection of consumers in various industries, including the payday loan sector. These regulations are designed to create a level playing field and prevent predatory lending practices that can often result in financial exploitation and debt traps for vulnerable borrowers. By establishing guidelines and restrictions on interest rates, loan terms, and the overall operations of lending institutions, governments aim to safeguard consumer interests and promote fair lending practices.

One of the main objectives of government regulations is to limit the exorbitant interest rates charged by payday loan lenders. Often, these loans come with sky-high interest rates that can reach triple-digit percentages, placing borrowers at a significant disadvantage. By implementing interest rate caps and restrictions, governments can help prevent borrowers from falling into a cycle of perpetual debt caused by these predatory lending practices. Additionally, regulations can also address issues such as loan rollovers and repayment terms, ensuring that borrowers are not trapped in a never-ending cycle of borrowing and repayment.

Educating Yourself on Responsible Borrowing and Budget Management

Responsible borrowing and effective budget management are crucial skills that can have a lasting impact on your financial well-being. By educating yourself on these topics, you can make informed decisions and avoid falling into the trap of excessive debt.

One of the first steps in educating yourself about responsible borrowing is to understand your financial situation. This involves analyzing your income, expenses, and existing debts. By creating a comprehensive budget, you can identify areas where you can cut back on expenses and allocate funds towards repaying your debts. Additionally, it is important to resist the temptation of borrowing beyond your means. Before taking on any new debt, carefully assess whether you can realistically afford the payments and if the purchase is truly necessary.

Another key aspect of responsible borrowing is being knowledgeable about the terms and conditions of any loan or credit agreement. Take the time to read and understand the fine print, including interest rates, repayment terms, and any additional fees. This will enable you to make informed decisions and avoid being caught off guard by unexpected costs. Additionally, it is essential to research and compare different lending options to ensure that you are getting the best possible terms and rates.

In conclusion, educating yourself on responsible borrowing and budget management is an essential step towards establishing financial stability. By understanding your financial situation, making informed decisions, and being aware of the terms and conditions of any borrowing, you can safeguard your financial well-being and avoid the potential pitfalls of excessive debt.

Recognizing the Importance of Credit Counseling and Financial Education

Credit counseling and financial education are invaluable resources for individuals seeking to improve their financial well-being. These services provide guidance, support, and knowledge that can help individuals make informed financial decisions and avoid common pitfalls.

Credit counseling, provided by certified professionals, offers personalized advice on debt management, budgeting, and financial planning. Through one-on-one sessions, credit counselors assess individuals’ financial situations, identify areas of improvement, and devise customized plans to address debt and financial challenges. They also provide education on responsible credit use, helping individuals understand the impact of their financial decisions and providing strategies to establish and maintain good credit. This guidance can be particularly beneficial for those struggling with debt or facing financial difficulties, as it empowers them to regain control over their financial lives.

On the other hand, financial education programs aim to equip individuals with fundamental financial skills and empower them to make wise financial choices. These programs often cover topics such as budgeting, saving, investing, and understanding credit. By increasing individuals’ financial literacy, these programs not only help them manage their day-to-day finances more effectively but also enable them to plan for their long-term financial goals, such as buying a home or saving for retirement. Moreover, financial education can help individuals become more resilient to financial shocks and better equipped to handle unexpected expenses or emergencies.

By recognizing the importance of credit counseling and financial education, individuals can take proactive steps towards improving their financial situation. These services can provide the knowledge and skills necessary to navigate the complex world of personal finance and achieve long-term financial stability. Whether facing debt, planning for the future, or simply seeking to enhance financial literacy, seeking out credit counseling and engaging in financial education can greatly impact individuals’ financial well-being and pave the way for a healthier financial future.

Examining the Consequences of Defaulting on Payday Loans

Defaulting on a payday loan can have severe consequences for borrowers. When a borrower fails to repay their loan in full and on time, they may be subjected to additional fees and charges. These fees can quickly accumulate, making the total repayment amount much higher than the initial loan amount. In addition to the financial impact, defaulting on a payday loan can also damage a borrower’s credit score and history, making it more difficult for them to obtain future loans or credit.

Defaulting on a payday loan can also result in harassment from debt collectors. These collectors may use aggressive tactics to recoup the outstanding debt, such as constant phone calls, emails, or even threats of legal action. This harassment can be extremely stressful and overwhelming for borrowers, further exacerbating their financial difficulties. It is essential for borrowers to be aware of the potential consequences of defaulting on a payday loan and to take steps to avoid it whenever possible.

Empowering Consumers: Tips for Safeguarding Your Financial Well-being

In today’s fast-paced world, safeguarding your financial well-being is crucial for long-term stability and success. Empowering yourself with the right knowledge and tools can help you make informed decisions and avoid financial pitfalls. Here are a few tips to keep in mind:

Firstly, it is essential to create and stick to a budget. Understanding your income, expenses, and financial goals will help you prioritize your spending and save for the future. Tracking your expenses, whether through a spreadsheet or a budgeting app, can give you a clear picture of where your money is going and where you may need to make adjustments.

Secondly, staying informed about your credit score is vital. Your credit score plays a significant role in loan eligibility, interest rates, and even job applications. Regularly checking your credit report for inaccuracies and paying your bills on time can help maintain a positive credit history. Additionally, limiting the amount of debt you carry and keeping your credit utilization low can further boost your credit score.

By implementing these tips into your financial habits, you can take control of your financial well-being and ensure a secure future. Remember, empowering yourself with knowledge and making responsible decisions are key to safeguarding your financial health.