Understanding the payday loan industry: A comprehensive overview

The payday loan industry has seen significant growth in recent years, with more and more individuals looking for quick and accessible financial solutions. Payday loans are short-term loans that are typically repaid within a month, often with high interest rates and fees attached. These loans are designed to provide immediate cash to individuals facing unexpected expenses or struggling to make ends meet between paychecks.

One of the key features of payday loans is their accessibility and convenience. Unlike traditional loans from banks or credit unions, payday loans do not require extensive credit checks or collateral. This makes them an attractive option for individuals with a poor credit history or those who do not own assets to secure a loan. However, it is important to understand that payday loans come with certain risks and challenges that need to be carefully considered before making a decision.

Key factors to consider when choosing a payday loan provider

When considering a payday loan provider, there are a few key factors that should be taken into account. First and foremost, it is important to evaluate the lender’s reputation and credibility. Look for providers that have been in the industry for a significant amount of time and have a solid track record of customer satisfaction. Checking online reviews and ratings can be a helpful tool in determining the reputation of a payday loan company.

Another crucial factor to consider is the interest rates and fees charged by the lender. Payday loans are known for their high interest rates, so it is important to compare rates among different providers to ensure you are getting the best deal possible. Additionally, be sure to carefully read the fine print and understand any additional fees that may be associated with the loan. Hidden fees can quickly add up and make the loan more expensive than initially anticipated.

Choosing a payday loan provider requires careful consideration and evaluation of various factors. By ensuring the lender has a good reputation and understanding the interest rates and fees charged, borrowers can make a more informed decision and minimize potential financial risks.

Examining the eligibility criteria for payday loans

To obtain a payday loan, borrowers must meet certain eligibility criteria set by the lenders. These criteria usually include age requirements, proof of a steady source of income, and a valid bank account. First and foremost, borrowers must be at least 18 years old, as payday loans are strictly intended for adults. This age requirement ensures that borrowers are legally responsible for the loan and have the capacity to enter into a financial agreement.

Additionally, payday loan providers require borrowers to demonstrate a source of income. This is an essential criterion as it reassures lenders that the borrower will be able to repay the loan on time. Valid sources of income can include employment income, government benefits, or even regular child support payments. By requiring proof of income, lenders minimize the risk of lending to individuals who cannot afford to repay the loan.

Furthermore, borrowers are typically required to have a valid bank account. This requirement serves as a means for lenders to disburse the loan amount and collect repayments electronically. Having a bank account also allows lenders to verify the borrower’s financial stability and track their repayment history. Overall, meeting the eligibility criteria for payday loans helps ensure that both borrowers and lenders enter into a responsible lending relationship.

The application process for payday loans: An in-depth guide

To apply for a payday loan, there are a few essential steps that need to be followed. Firstly, you will need to gather all the necessary documentation, which typically includes proof of identification, proof of income, and proof of address. It is crucial to ensure that these documents are valid and up to date, as they will be used to assess your eligibility for the loan.

Once you have gathered all the required documents, the next step is to complete the application form provided by the payday loan provider. This form will usually ask for personal information, such as your name, contact details, employment information, and banking details. Make sure to fill in all the fields accurately and truthfully, as any discrepancies may lead to delays or rejection of your application. After completing the form, carefully review it to ensure that there are no errors or missing information. Finally, submit the application along with the supporting documents.

Assessing the transparency and credibility of payday loan companies

Companies that operate within the payday loan industry are often subject to scrutiny due to the nature of their business. As borrowers often find themselves in vulnerable financial situations, it is crucial to assess the transparency and credibility of payday loan companies to ensure they can be trusted. Transparency is of utmost importance in this industry, as it involves dealing with individuals who may already be experiencing financial hardship. Reputable payday loan providers will clearly outline all terms and conditions of the loan, including interest rates, fees, repayment options, and any potential penalties that may be incurred. This level of transparency allows borrowers to make informed decisions and understand the true cost of borrowing.

Credibility is another crucial aspect to consider when assessing payday loan companies. A credible payday loan provider will be properly licensed and regulated by the appropriate authorities. They will have a clear and well-established track record, with positive feedback and testimonials from previous borrowers. Additionally, credible companies will have a professional and responsive customer service team that is readily available to address any queries or concerns borrowers may have. By considering both transparency and credibility, borrowers can ensure they are dealing with a trustworthy payday loan company that is committed to providing fair and reliable financial solutions.

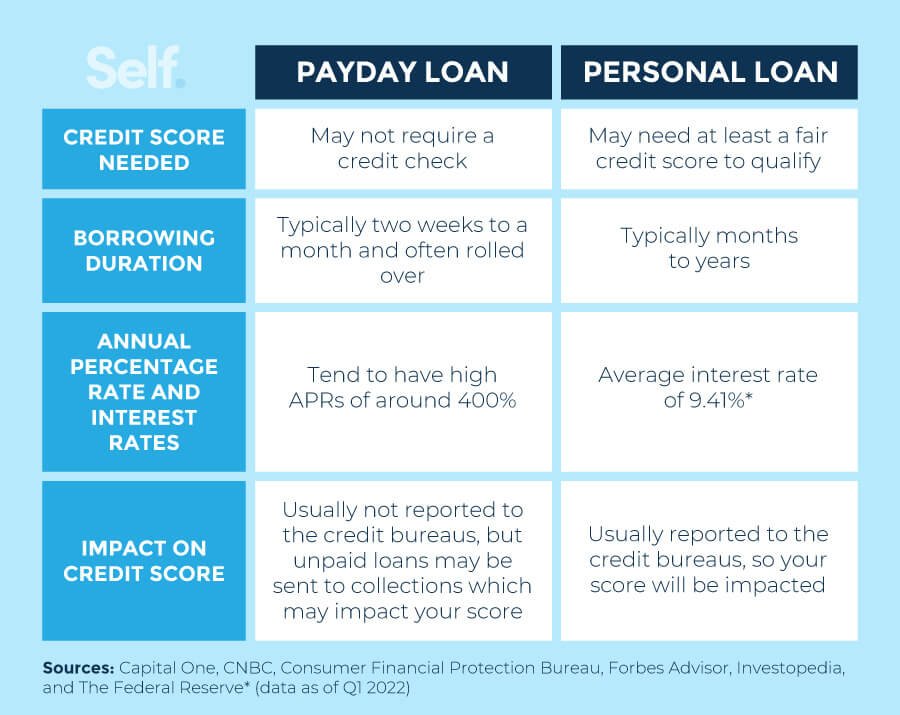

Comparing interest rates and fees among different payday loan providers

When considering payday loan providers, it is essential to explore and compare the interest rates and fees associated with each option. These costs can vary significantly among different lenders, and understanding them is crucial to making an informed decision. By taking the time to compare the interest rates and fees across various payday loan providers, borrowers can ensure they are selecting a loan option that best fits their financial needs.

Interest rates are one of the primary factors to consider when comparing payday loan providers. Typically, these rates are expressed as an annual percentage rate (APR), which represents the cost of borrowing over one year. While payday loans are typically short-term loans, the APR can still provide useful insight into the overall cost of borrowing. Additionally, it is essential to examine any additional fees or charges that may be levied by the lender, such as origination fees or late payment penalties. Evaluating these fees alongside the interest rates will allow borrowers to determine the total cost of the loan and make an informed decision.