The Basics of Payday Loans: Exploring Short-Term Financing Options

Payday loans are a type of short-term financing that can provide quick cash when you’re facing a financial emergency. These loans are typically for small amounts, usually ranging from $100 to $1,000, and are meant to be repaid within a short timeframe, usually within a few weeks or on your next payday. They are designed to be a temporary solution to help bridge the gap between paydays.

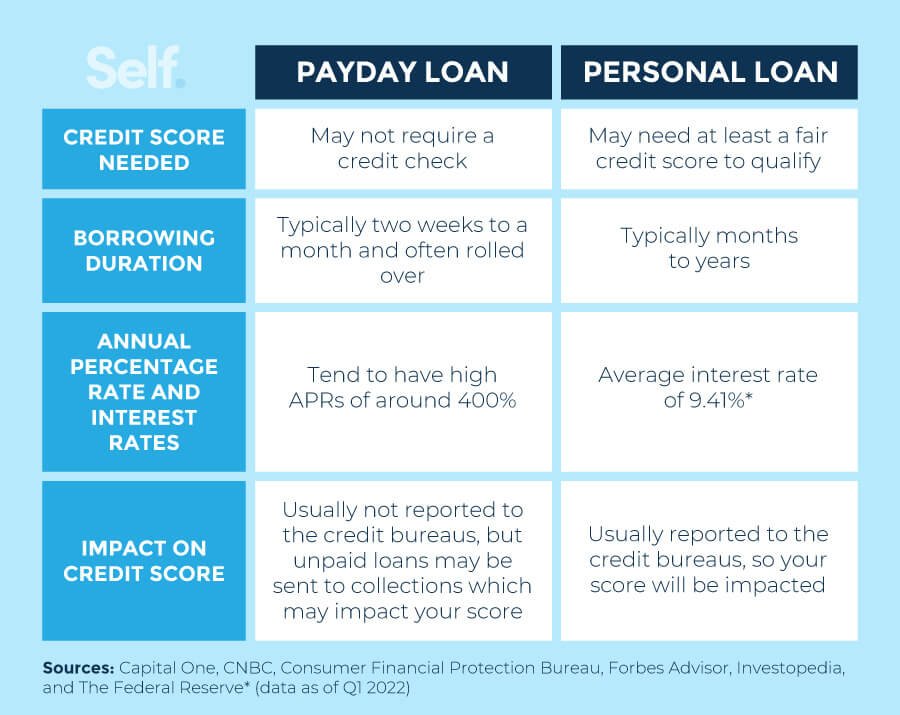

One of the key features of payday loans is their accessibility. Unlike traditional loans from banks or credit unions, payday loans don’t require a lengthy application process or a good credit score. In fact, many payday lenders don’t even perform a credit check. This makes payday loans an option for individuals with poor or no credit history who may not qualify for other types of loans. However, it’s important to note that payday loans often come with high interest rates and fees, so it’s crucial to carefully consider the costs before taking out a payday loan.

How Payday Loans Work: Understanding the Borrowing Process

When considering a payday loan, it is essential to understand the borrowing process. Payday loans are short-term loans that typically range from $100 to $1,500. The borrowing process usually involves a few simple steps. First, the borrower completes an application form, providing personal and financial information. This information helps the lender assess the applicant’s eligibility for the loan. Once the application is submitted, the lender will evaluate it, considering factors such as income, employment status, and credit history. If approved, the borrower will receive the loan amount, usually deposited directly into their bank account. Repayment is then typically due on the borrower’s next payday, with the loan amount plus any applicable fees and interest. It is important to note that payday loans usually have high-interest rates and short repayment terms, making them a costly borrowing option for many individuals.

Key Features of Payday Loans: Interest Rates, Fees, and Repayment Terms

Interest rates, fees, and repayment terms are key features that borrowers should carefully consider when taking out a payday loan. These factors determine the overall cost of borrowing and can have a significant impact on an individual’s financial situation.

Firstly, payday loans typically come with high interest rates compared to traditional loans. Lenders charge a fixed fee based on the amount borrowed, which is due to be repaid on the borrower’s next payday. This fee can vary depending on the lender and the state regulations, but it often equates to a high annual percentage rate (APR).

In addition to the high interest rates, borrowers should be aware of the fees associated with payday loans. Lenders may charge application fees, administrative fees, or late payment fees, which can quickly add up and increase the overall cost of the loan. It is crucial to thoroughly read the terms and conditions before signing an agreement to understand all the fees involved.

Repayment terms for payday loans are typically short, ranging from a few days to a few weeks. Unlike traditional loans with monthly installments, payday loans require borrowers to repay the entire amount borrowed, along with the fees and interest, in one lump sum on the due date. This can be challenging for individuals who are already facing financial difficulties and may lead to a cycle of borrowing to repay the loan.

Understanding the interest rates, fees, and repayment terms of payday loans is essential to make an informed borrowing decision. It is crucial to carefully evaluate whether the cost of borrowing is reasonable and manageable within one’s financial circumstances. Exploring alternative options and seeking financial advice can also help individuals find better alternatives to payday loans that offer more affordable terms.

Eligibility Criteria for Payday Loans: Who Can Apply and What are the Requirements?

To be eligible for a payday loan, there are a few criteria that applicants must meet. First and foremost, individuals must be at least 18 years old and have a valid government-issued ID. This ensures that borrowers are of legal age and can be identified for verification purposes. Additionally, applicants are generally required to have a steady source of income. This could include regular employment, government benefits, or other forms of verifiable income. By having a consistent source of funds, lenders can assess whether borrowers have the means to repay the loan amount plus any associated fees. Lastly, borrowers must have an active checking account. This is typically where the lender will deposit the loan funds and where they will automatically withdraw the repayment on the agreed-upon date. Having a checking account allows for a seamless transfer of funds, making the borrowing process more convenient for both parties involved.

Aside from these basic requirements, payday loan lenders may have additional eligibility criteria that borrowers must meet. These can vary depending on the lender and the specific loan terms. Some lenders may require a minimum credit score, while others may conduct a background check. It’s essential for individuals considering a payday loan to carefully review the lender’s eligibility criteria before applying to ensure they meet all the necessary requirements. This can help save time and prevent potential disappointment if an application is ultimately rejected due to a failure to meet specific criteria.

Pros and Cons of Payday Loans: Weighing the Benefits and Risks

Payday loans can be a helpful financial tool for individuals facing emergency expenses or unexpected bills. One of the primary benefits of payday loans is their accessibility and convenience. Unlike traditional loans from banks or credit unions, payday loans do not require a lengthy application process or a high credit score. This makes them a viable option for individuals with a poor credit history or those who need funds quickly.

Another advantage of payday loans is that they provide immediate financial relief. When faced with an urgent expense, such as a medical bill or car repair, a payday loan can provide the necessary funds to address the situation promptly. The quick application and approval process allow borrowers to have access to cash within a short period, providing peace of mind in times of financial stress. Additionally, payday loans are typically unsecured, meaning borrowers do not need to provide collateral, such as a car or property, to secure the loan. This reduces the risk of losing valuable assets in case of non-payment.

Alternatives to Payday Loans: Exploring Safer and More Affordable Options

When faced with a financial emergency, it’s important to consider alternatives to payday loans that offer safer and more affordable options. One alternative is to explore community resources and assistance programs. Many organizations and nonprofits provide financial counseling, budgeting assistance, and emergency support to help individuals in need. These resources can provide valuable guidance and help individuals find sustainable solutions to their financial challenges.

Another alternative to payday loans is to consider borrowing from friends or family. While it can be difficult to ask for financial support from loved ones, it can be a more affordable option compared to high-interest payday loans. Prioritize open communication and transparency when discussing the terms of the loan, including repayment plans and any interest that may be involved. By approaching your loved ones with respect and honesty, you may be able to find a mutually beneficial solution that avoids the high costs and risks associated with payday loans.

Responsible Borrowing: Tips for Managing Payday Loans Effectively

When it comes to managing payday loans effectively, responsible borrowing is key. One important tip is to only borrow what you absolutely need and can afford to repay. It’s easy to get caught up in the cycle of borrowing larger sums each time, but this can lead to a never-ending cycle of debt. By carefully assessing your financial situation and borrowing only what is necessary, you can avoid falling into this trap.

Another tip for responsible borrowing is to carefully read and understand the terms and conditions of the payday loan before signing any agreements. Pay close attention to the interest rates, fees, and repayment terms. Make sure you are fully aware of how much you will be required to repay and when the repayment is due. This will help you avoid any surprises and ensure that you are able to make timely repayments. By being diligent in your research and understanding the terms, you can effectively manage your payday loan and avoid any unnecessary financial strain.

Understanding Payday Loan Regulations: How the Industry is Regulated

Payday loan regulations play a crucial role in overseeing the operations of the industry and protecting consumers from unfair lending practices. These regulations are put in place by government authorities to ensure that payday lenders adhere to certain guidelines and standards. One important aspect of payday loan regulations is the limitation on interest rates and fees that lenders can charge.

In many jurisdictions, there are specific caps on the maximum amount of interest and fees that can be charged on payday loans. These caps are designed to prevent lenders from exploiting vulnerable individuals in urgent financial situations. Additionally, regulations often require lenders to provide clear and transparent information about the cost of borrowing, including the annual percentage rate (APR). This ensures that borrowers have a clear understanding of the total cost of borrowing and can make informed decisions. Advance Information Systems (AIS) require lenders to disclose the loan’s APR, repayment terms, and any other relevant information at the time of application, making it easier for borrowers to compare different payday loan options.

Payday Loan Myths Debunked: Separating Fact from Fiction

Myth: Payday loans are a quick fix for financial emergencies.

Fact: While payday loans may provide immediate cash, they are not a long-term solution for financial emergencies. These loans typically come with extremely high-interest rates and fees, which can trap borrowers in a cycle of debt. It is important to carefully consider alternative options and develop a comprehensive financial plan to address emergency expenses.

Myth: Payday loans are easily accessible for everyone.

Fact: While payday loans may seem like a readily available option, not everyone is eligible to apply. Most lenders require borrowers to meet specific criteria, including having a stable source of income and a minimum age requirement. Additionally, payday loans may not be legal in all jurisdictions or may be heavily regulated. It is crucial to understand the eligibility requirements and applicable regulations before considering a payday loan as a financing option.

How to Avoid the Payday Loan Cycle: Building Financial Stability for the Future

Payday loans can often become a costly cycle, trapping borrowers in a never-ending cycle of debt. However, there are steps that individuals can take to avoid this cycle and build financial stability for the future. The first step is to carefully assess your financial situation and create a realistic budget. This can help you determine your income, expenses, and identify areas where you can cut back or save. By sticking to a budget, you can ensure that you have enough money to cover your living expenses and essential bills, reducing the need for payday loans.

Another important way to avoid the payday loan cycle is to build an emergency fund. Having a financial cushion can help you deal with unexpected expenses without resorting to payday loans. Start by setting aside a portion of your income each month and gradually build up your emergency fund. By having savings to fall back on, you can reduce the reliance on short-term loans and maintain financial stability in the long run. Additionally, it is crucial to explore other financial resources and options. Investigate local credit unions or community organizations that may offer low-interest loans or financial assistance programs. These alternatives can provide a safer and more affordable option compared to payday loans. By being proactive and seeking out other resources, you can avoid the payday loan cycle and establish a solid foundation for long-term financial stability.