Eligibility Criteria: Understanding the Qualifications for a Payday Loan

To be eligible for a payday loan, there are certain qualifications that borrowers must meet. First and foremost, you must be at least 18 years old and have proof of identification. This is to ensure that the borrower is of legal age and can be held responsible for the loan. Additionally, you will need to provide proof of income. This can be in the form of pay stubs, bank statements, or other documentation that shows you have a steady source of income. Lenders require this information to assess your ability to repay the loan on time.

Another important eligibility criterion is having an active and valid bank account. This allows the lender to deposit the loan funds directly into your account and to withdraw the repayment amount on the agreed-upon due date. It also verifies that you have a banking relationship and a means for repayments. Lastly, you need to be a resident of the state in which you are applying for the payday loan. Different states have varying regulations and restrictions on payday lending, so lenders need to confirm that you meet the residency requirements before approving your loan application. Understanding these qualifications is essential in determining whether or not you are eligible for a payday loan.

Application Process: Step-by-Step Guide to Applying for a Payday Loan

To apply for a payday loan, you’ll need to follow a step-by-step process. The first step is to research and choose a reputable lender. Make sure to read customer reviews and compare interest rates and fees. Once you’ve selected a lender, visit their website or go to their physical location to start the application process.

Next, you’ll need to provide personal and financial information. This includes your full name, contact information, employment details, and proof of income. Some lenders may also ask for references or your social security number for verification purposes. Be prepared to provide accurate and up-to-date documentation to ensure a smooth application process.

After submitting your application, the lender will review your information and determine whether you meet their eligibility criteria. If approved, you will receive a notification, usually within a few minutes or hours. Upon approval, you’ll need to carefully review the loan terms, including repayment schedules and interest rates. Make sure you understand all the terms and conditions before proceeding with the loan. Once accepted, the funds will be deposited into your bank account, typically within one business day.

Applying for a payday loan may seem straightforward, but it’s crucial to approach the process with caution and responsibility. Make sure to borrow only the amount you truly need and can comfortably repay. Payday loans are intended for short-term, emergency situations and should not be used as a long-term financial solution. By carefully considering your options and utilizing payday loans responsibly, you can effectively manage your financial needs while minimizing the risk of falling into a debt trap.

Required Documentation: Documents You Need to Provide for a Payday Loan Application

When applying for a payday loan, it is important to gather the necessary documentation to ensure a smooth and efficient application process. Lenders require certain documents to verify your identity, income, and other relevant information. These documents serve as proof of your ability to repay the loan and assist lenders in assessing your eligibility. The specific documents required may vary depending on the lender and your individual circumstances, but there are some common documents you will likely need to provide.

Firstly, you will typically be asked to provide a valid form of identification, such as a driver’s license or passport. This ensures that you are who you say you are and helps prevent fraud. Additionally, lenders will require proof of income, which may include recent pay stubs, bank statements, or tax returns. This documentation is used to verify your employment status and income level, as it is an essential factor in determining your loan amount and repayment ability. Depending on the lender, you may also need to provide proof of residency, such as utility bills or lease agreements. These documents help establish your current address and may be necessary for compliance purposes. By preparing these required documents in advance, you can streamline the application process and increase your chances of a successful loan approval.

Income Verification: How Lenders Verify Your Income for a Payday Loan

Lenders play a crucial role in ensuring the financial stability and credibility of borrowers when it comes to payday loans. One of their key responsibilities is to verify the income of the applicants. This verification process helps lenders determine whether the borrower has the capacity to repay the loan responsibly. It also aids in assessing the risk associated with the loan, ensuring that both parties are making informed decisions.

To verify income, lenders typically request documents such as pay stubs, bank statements, or tax returns. These documents serve as proof of the borrower’s income and allow the lender to calculate the borrower’s debt-to-income ratio. By analyzing this ratio, lenders can evaluate the borrower’s ability to manage their finances and make timely loan repayments. Additionally, some lenders may contact the borrower’s employer directly to verify employment status and income details, ensuring the accuracy of the provided documents. Overall, income verification is a crucial step in the payday loan application process, as it helps lenders make informed decisions and mitigate the risks involved.

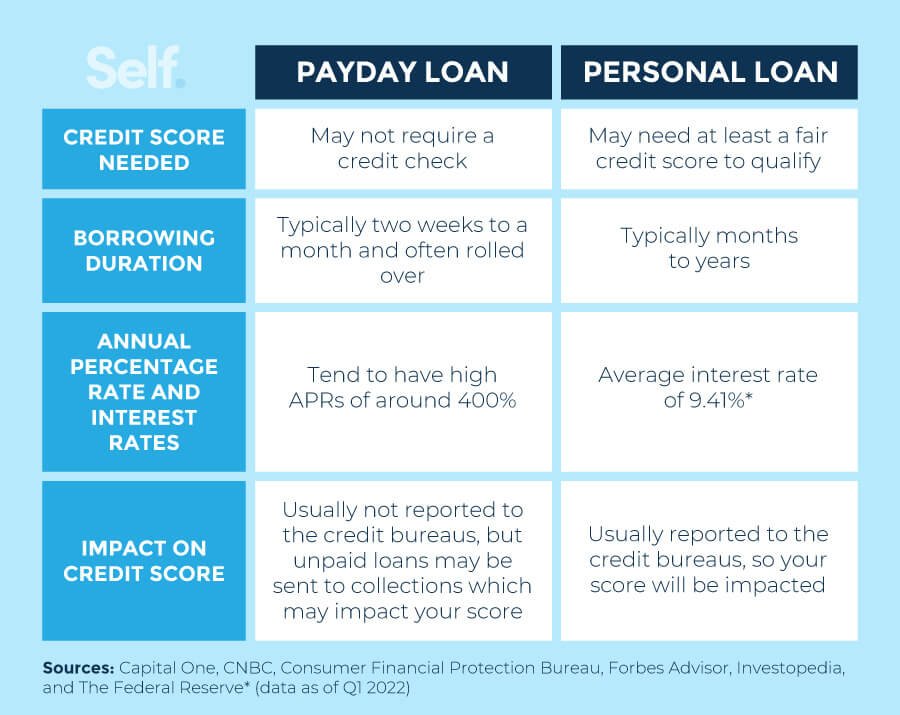

Credit Check: Exploring the Role of Credit History in Payday Loan Approval

For many people seeking a payday loan, the role of credit history in the approval process can be a major concern. Unlike traditional lenders, payday loan providers typically do not heavily rely on credit checks when determining eligibility. This means that even if you have a less-than-perfect credit score, you may still be eligible for a payday loan. Instead, lenders focus more on your income and ability to repay the loan on time. This can be a relief for those who have struggled with credit issues in the past and are in need of quick financial assistance. However, it is important to keep in mind that while credit history may not be the primary factor in payday loan approval, it can still be considered by some lenders. It is always a good idea to be well-informed about your credit history and take steps to improve it if necessary.

To apply for a payday loan, you will typically need to provide certain documentation and information to the lender. This may include proof of identification, such as a valid ID or driver’s license, as well as proof of income, such as recent pay stubs or bank statements. In some cases, lenders may also request proof of residence, such as utility bills or lease agreements. By verifying these documents, lenders can gain a better understanding of your financial situation and make an informed decision regarding your loan application. It is important to ensure that all the required documentation is accurate and up to date, as any discrepancies or incomplete information may delay the approval process.

Loan Repayment: Understanding Repayment Options and Terms for Payday Loans

Payday loans, often used as a short-term solution for financial emergencies, come with repayment options and terms that borrowers need to understand before taking on the loan. Repayment options for payday loans typically involve either a lump sum payment or multiple installments over a set period. The terms of repayment can vary depending on the lender and the amount borrowed, so it is crucial for borrowers to carefully read and comprehend the loan agreement. It is important to note that failing to meet the repayment terms may lead to additional fees and penalties, and can also have a negative impact on the borrower’s credit history.

When it comes to payday loan repayment, borrowers should be aware of any fees and interest rates associated with the loan. Generally, payday loans tend to have relatively high interest rates compared to traditional loans. These rates can vary depending on factors such as the borrower’s credit history, income, and the amount borrowed. It is important for borrowers to consider these costs and determine if they can afford to repay the loan in full, along with any additional fees, by the agreed-upon due date. Understanding the repayment options and terms of payday loans is essential in order to make informed decisions and avoid falling into a cycle of debt.

Interest Rates and Fees: Explaining the Costs Associated with Payday Loans

Payday loans are known for their high interest rates and fees, which can quickly add up and make these loans quite expensive. The interest rates for payday loans are typically much higher than traditional bank loans or credit cards, often ranging from 300% to 600% APR (Annual Percentage Rate). This means that if you borrow $500 for two weeks, you may end up owing $575 or more when it comes time to repay the loan.

In addition to the interest rates, payday loans also come with various fees. These fees can include application fees, processing fees, late payment fees, and even fees for extending or renewing the loan. It’s important to carefully review the terms and conditions of the loan before signing any agreement, as these fees can significantly impact the overall cost of borrowing.

Borrowing Limits: How Much Money Can You Borrow with a Payday Loan?

Payday loans offer a quick and convenient solution for individuals facing unexpected financial emergencies. However, it is important to understand the borrowing limits associated with these loans. The amount of money you can borrow with a payday loan typically varies based on several factors, including the state regulations, the lender’s policies, and your income level.

In general, payday loans are designed to provide small, short-term cash advances. As a result, the borrowing limits for payday loans are usually lower compared to traditional bank loans. The maximum amount you can borrow typically ranges from $100 to $1,000, depending on the lender and your income level. It is crucial to carefully assess your financial needs and borrow only what you can afford to repay, as payday loans often come with high interest rates and fees. Additionally, most lenders will evaluate your income and financial stability to determine the maximum amount they are willing to lend you.

Alternatives to Payday Loans: Exploring Other Options for Emergency Cash

When faced with a financial emergency, payday loans may seem like a quick and easy solution. However, it is important to explore other alternatives before committing to such high-cost borrowing. One option to consider is applying for a personal loan from a traditional bank or credit union. These institutions often offer lower interest rates and more flexible repayment terms compared to payday lenders. Additionally, you can also explore borrowing from friends or family, or even reaching out to local charitable organizations for assistance. By exploring these alternatives, you can potentially find a more affordable and sustainable solution to your emergency cash needs, while avoiding the high costs associated with payday loans.

Another alternative to payday loans is to utilize a credit card or line of credit if you have one available. While it is important to be cautious with credit card use, as high interest rates can also be problematic, using a credit card can still be a more cost-effective option compared to a payday loan. Additionally, you can explore whether you are eligible for an overdraft facility on your bank account, as this can provide you with temporary access to funds in case of emergencies. Finally, if your emergency is related to essential living expenses such as rent or utilities, it may be worth contacting your service providers to discuss payment plans or extensions. Many companies are willing to work with customers facing temporary financial difficulties, providing a more manageable solution than taking out a payday loan.

Responsible Borrowing: Tips for Using Payday Loans Wisely and Avoiding Debt Traps

It is important to approach payday loans with caution and use them responsibly to avoid falling into a cycle of debt. Before applying for a payday loan, evaluate your financial situation and determine if it is the best option for your needs. Consider if there are alternative ways to address your emergency cash needs, such as borrowing from friends or family, using credit cards, or seeking assistance from community organizations.

When using a payday loan, it is crucial to borrow only what you can afford to repay within the specified time frame. Carefully review the terms and conditions, including interest rates and fees, to understand the total cost of borrowing. It is advisable to only take out a payday loan for essential expenses and not for unnecessary purchases. By responsible borrowing and timely repayment, you can effectively use payday loans as a temporary solution during financial emergencies.