State Regulations on Payday Loans

Payday loans, also known as cash advances or paycheck advances, are short-term loans typically taken out by individuals in need of immediate funds. However, the regulation of these loans varies from state to state. Some states have implemented strict regulations to protect consumers, while others have more lenient laws in place.

In states with stricter regulations, payday lenders are required to adhere to certain guidelines regarding loan amount limits, interest rates, and repayment terms. These regulations aim to prevent borrowers from falling into a cycle of debt by restricting the amount of money they can borrow and implementing caps on interest rates. Additionally, some states require lenders to offer repayment plans or installment options to help borrowers repay their loans in a more manageable manner. By implementing these regulations, states are working to ensure the fair treatment of consumers in the payday loan industry.

Legal Restrictions on Payday Lending

Payday lending, a controversial industry that offers short-term loans with high interest rates, is subject to legal restrictions in many states across the United States. These regulations aim to protect consumers from the potential pitfalls of payday loans, such as escalating debt and predatory lending practices.

One common legal restriction is the establishment of a maximum loan amount that lenders are permitted to offer. This ensures that borrowers do not take on excessive debt that they may struggle to repay. Additionally, interest rates and fees charged by payday lenders are often regulated to prevent exorbitant charges that can exacerbate borrowers’ financial difficulties. By implementing these restrictions, states aim to strike a balance between providing access to credit for those in need and safeguarding consumers from exploitation.

Consumer Protection Laws for Payday Loans

Laws and regulations regarding payday loans vary from state to state, with the aim of protecting consumers from predatory lending practices. In order to ensure fairness and transparency, many states have implemented specific requirements for lenders operating within their jurisdiction. These requirements often include provisions such as loan amount limits, caps on interest rates and fees, and mandatory borrower education.

One common consumer protection measure is the establishment of a maximum loan amount that lenders can provide. This is typically based on the borrower’s income and may vary depending on the state in which the payday loan is issued. By setting a cap on the loan amount, states aim to prevent borrowers from becoming trapped in an unmanageable cycle of debt. Additionally, interest rates and fees charged by payday lenders are often regulated to avoid excessive charges that could further burden borrowers. These measures help protect consumers from lending practices that could potentially exploit their financial vulnerabilities.

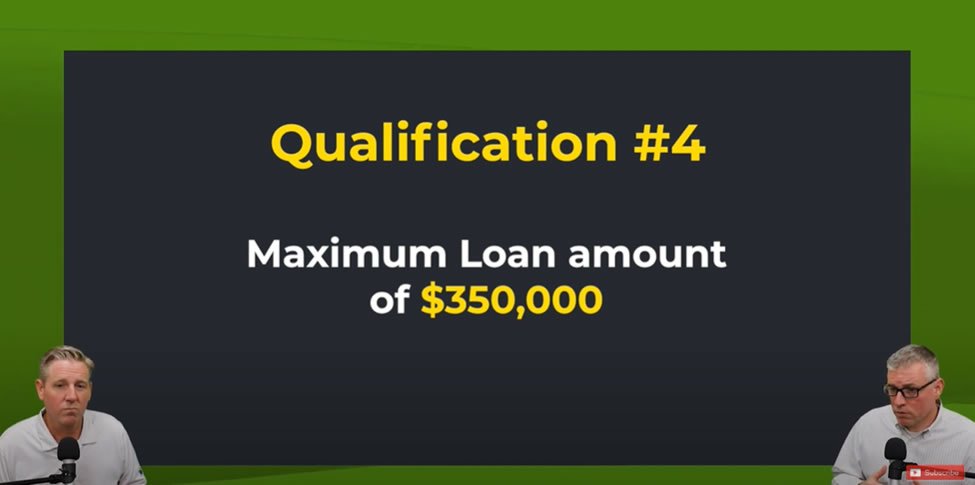

Maximum Loan Amounts in Each State

In the realm of payday lending, each state has its own set of regulations dictating the maximum loan amounts that can be issued. These regulations serve as a safeguard, aiming to protect borrowers from becoming trapped in a cycle of debt. The maximum loan amount varies considerably across states, ranging from as low as $300 to as high as $1,500.

States such as California, Texas, and Illinois have implemented a maximum loan amount of $300, ensuring that borrowers are not overly burdened with an excessive amount of debt. On the other end of the spectrum, states like Delaware, Utah, and Wisconsin allow for a maximum loan amount of $1,500, providing borrowers with greater flexibility in meeting their financial needs. These varying loan limits reflect the diverse approaches taken by states to strike a balance between ensuring access to credit and protecting consumers from predatory lending practices.

Interest Rates and Fees for Payday Loans

In the realm of payday loans, interest rates and fees play a critical role in determining the overall cost of borrowing. These rates and fees can vary significantly depending on state regulations and the specific lender. It is essential for borrowers to have a clear understanding of the terms and conditions associated with these financial products before entering into any agreement.

When it comes to interest rates, payday loans often carry higher rates compared to traditional bank loans. This is primarily due to the short-term nature of these loans and the increased risk for lenders. Fees are another component of the cost associated with payday loans. These may include origination fees, processing fees, or late payment charges. It is crucial for borrowers to carefully review and compare the interest rates and fees offered by different lenders to ensure they are making an informed decision. By doing so, individuals can minimize the potential financial burden associated with these types of loans.

Repayment Terms and Options for Borrowers

One aspect that borrowers should carefully consider when taking out a payday loan is the repayment terms offered by the lender. Typically, these loans have a short repayment period, ranging from a few weeks to a month. Additionally, lenders often require borrowers to repay the loan in full, including interest and fees, by their next payday.

It is crucial for borrowers to fully understand the repayment options available to them. Some lenders may allow borrowers to extend the repayment period by paying an additional fee, while others may offer installment plans. However, it is important to note that these options may come with additional costs, and borrowers should carefully weigh the potential effects on their finances before making a decision. Ultimately, borrowers should strive to enter into payday loan agreements that align with their ability to repay on time and in full.